Controllers of controlled foreign companies, attention!

State Tax Service of Ukraine focuses attention of controllers of controlled foreign companies on the need to reflect complete information in reports on controlled foreign companies.

Order of the Ministry of Finance of Ukraine № 254 as of 25.08.2022, registered in the Ministry of Justice on 11.10.2022 under № 1219/38555, approved the form of Report on controlled foreign companies, form of the abbreviated Report on controlled foreign companies, procedure for filling out Report on controlled foreign companies, abbreviated forms of Report on controlled foreign companies and submission to the controlling body.

Paragraph 392.5 Article 392 Section I of the Tax Code of Ukraine (hereinafter – Code) establishes requirements for preparation and submission of Report on controlled foreign companies, in particular, it is determined that Report on controlled foreign companies is submitted to the controlling body simultaneously with submission of annual property and income declaration or corporate income tax declaration for relevant calendar year by electronic communication means in electronic form in compliance with requirements of the laws of Ukraine "On electronic documents and electronic document management" and "On electronic identification and electronic trust services".

In the Taxpayer's electronic cabinet, there is Report on controlled foreign companies with the form identifier: J0108701 – for legal entities and F0108701 – for individuals.

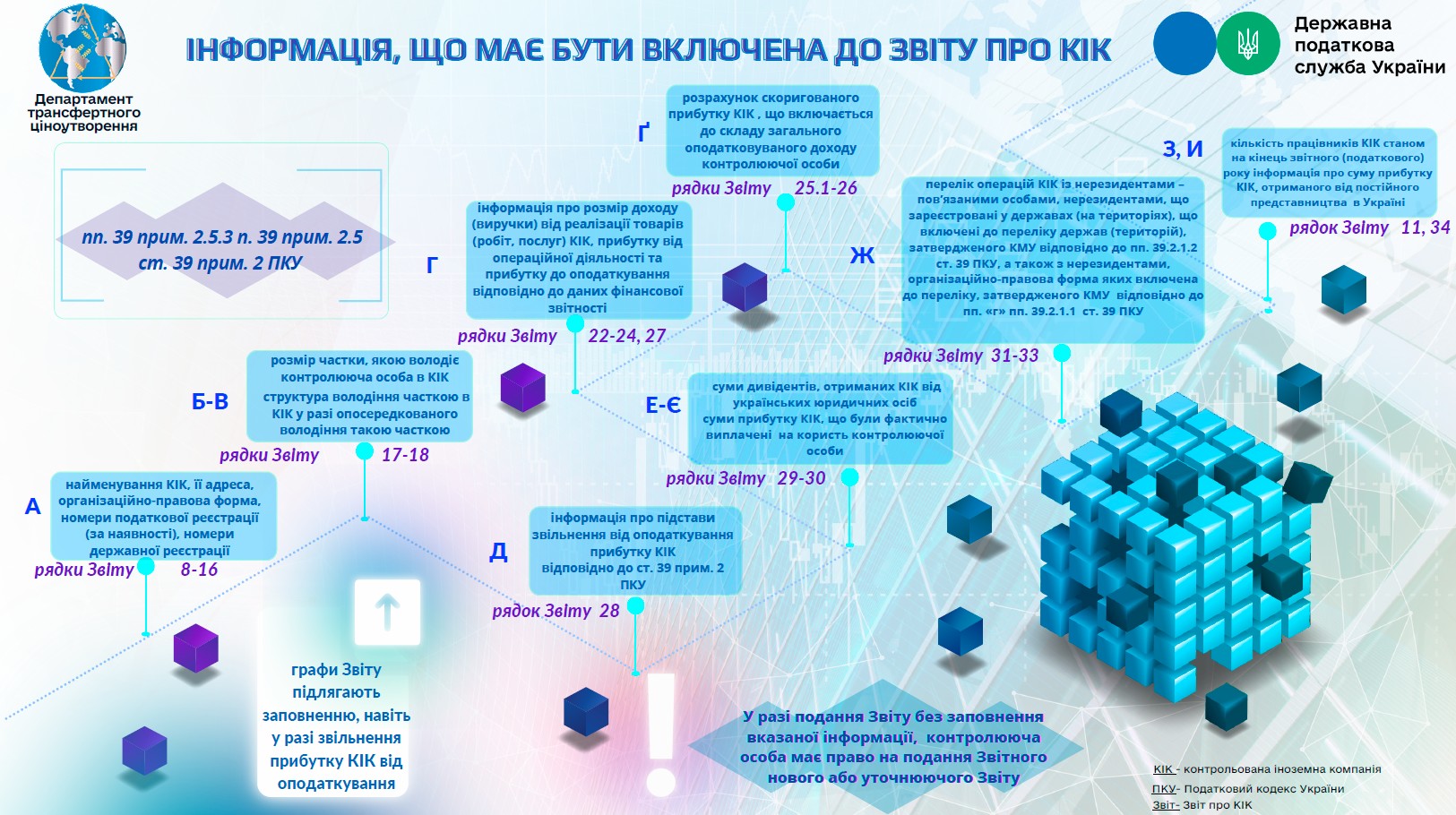

Sub-paragraph 392.5.3 Paragraph 392.5 Article 392 Section I of the Code defines list of information that must be noted in report.

At the same time, provisions of Paragraph 392.4 Article 392Section I of the Code provide list of conditions, in case of compliance with which adjusted profit in Report on controlled foreign companies is not included in tax base of the controlling entity.

At the same time, according to Sub-paragraph 392.4.3 Paragraph 392.4 Article 392 Section I of the Code, if profit of controlled foreign companies is exempted from taxation according to provisions of this Paragraph, the controlling entity is released from obligation to calculate adjusted profit of controlled foreign companies.

Please note that the Code does not establish separate rules or exceptions for the taxpayer - controlling entity regarding non-reflection in Report on controlled foreign companies of information defined, in particular, by Sub-paragraphs "e", "e", "z", "y" of Sub-paragraph 392.5.3 Paragraph 392.5 Article 392 of the Code, and therefore, such information is subject to reflection in relevant columns of Report on controlled foreign companies (columns 29 - 34).

In case of exemption from taxation of income of the controlled foreign companies according to requirements of Paragraph 392.4 Article 392 of the Code, there are no legal grounds for not reflecting in Report on controlled foreign companies information specified in Sub-paragraphs "e", "e", "g", "y" of Sub-paragraph 392.5.3 Paragraph 392.5 of Article 392 of the Code.

At the same time, responsibility for violation of requirements of the Code regarding non-reflection of information in Report on controlled foreign companies is determined by Paragraph 120.7 Article 120 of the Code.

Separately, please note that Article 50 of the Code gives the controlling entity right to submit new or clarifying report on controlled foreign companies.